“Our accountant never mentioned the FICA tip credit. They found three years of unclaimed credits. That $124,000 went straight into renovating our patio.”

Carlos M.

Owner, Latin Cuisine Restaurant

$0K

Amount recovered ✅

What Would You Do With a $10k–$250k+ Tax Refund?

TippedRefund.com exists for one reason: getting hospitality business owners their FICA Tip Credit Refunds sitting unclaimed at the IRS. Our application process takes just 4 minutes. No digging through boxes of payroll reports or old tax returns. We only get paid when you get paid, so there's $0 upfront cost. Apply now to lock in your priority processing spot.

No tax refund? No cost

As seen on the following news networks:

100 % IRS-compliant

Over $1B+ in claims

Helped 10k+ businesses

Encrypted digital platform

50 states covered

Success fee only

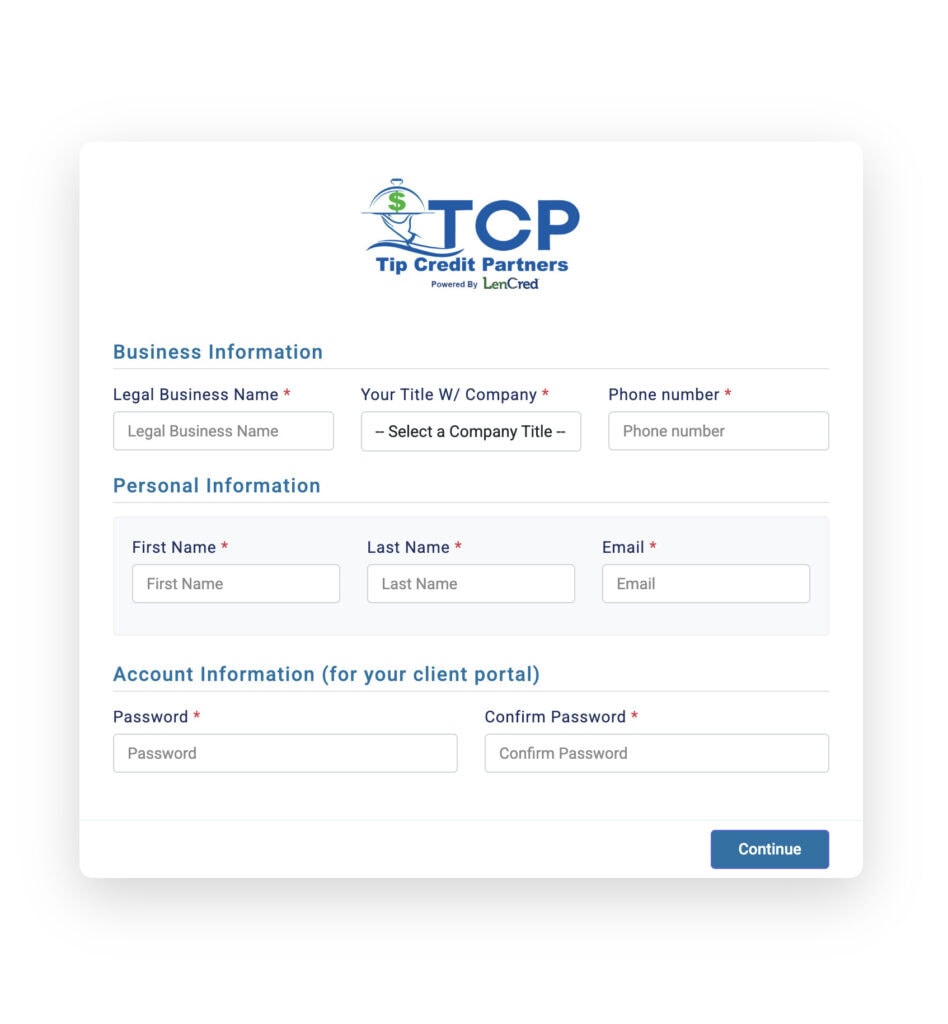

Enter your restaurant or bar details below to estimate your FICA tip credit refund. This is just a quick estimate. We'll calculate your actual credit automatically from your official payroll and tax records during the application process.

How many tipped employees are currently on your team?

Roughly how much does one server earn in tips per week?

Checking against §45B Credit Guidelines

Total Potential Cash Refund (3 Years)

*This is an estimate. Your actual refund is calculated from official payroll data during the secure application process. Not tax advice.

Food and beverage business owners across the US and Puerto Rico have claimed FICA Tip Credit Refunds worth five and six figures. The average refund for TippedRefund.com clients lands at around $50,000. Some recover $250,000+. See examples of successful claims below.

“Our accountant never mentioned the FICA tip credit. They found three years of unclaimed credits. That $124,000 went straight into renovating our patio.”

Amount recovered ✅

“As a small bar owner, I was skeptical, but they delivered exactly what they promised. $18,500 back in my pocket with zero hassle.”

Amount recovered ✅

“We assumed credits like this were only for larger chains. Turns out our 40-seat bar qualified for over $130,000. A couple of clicks, done.”

Amount recovered ✅

“I run a laid-back spot with a small crew. We found $91,000 in unclaimed credits. I had the money in my account within 60 days.”

Amount recovered ✅

“We recovered more than $45,000 in tax credits we had no idea existed. The entire process required almost nothing from our team.”

Amount recovered ✅

“We’d been missing out on this credit for years. They helped us claim retroactively and secured over $60,000 in credits. Game-changer for our business.”

Amount recovered ✅

No tax refund? No cost

Your hospitality business qualifies for the FICA Tip Credit Refund if it meets the following 4 IRS criteria.

Full-service restaurants qualify for the FICA Tip Credit. Servers take orders and deliver food to guests at their tables. Eligible examples: steakhouses, Italian restaurants, and diners.

Bars and nightclubs meet the IRS eligibility requirements. Bartenders and servers regularly receive tips from patrons. Eligible examples: sports bars, cocktail lounges, nightclubs, and pubs.

Hotels and resorts can claim the FICA Tip Credit. Bellhops, room service staff, and concierges receive gratuities from guests. Eligible examples: luxury hotels, boutique properties, and motels.

A lot of catering companies qualify for the FICA tax credit. Staff receive tips when serving food at off-site functions. Eligible examples: wedding caterers, corporate event providers, and private chefs.

Coffee shops and cafes count among eligible businesses for the FICA Tip Credit. Baristas and counter staff accept tips for beverage and light meal service. Eligible examples: coffee houses, bakery cafes, and breakfast spots.

Any establishment where employees customarily receive gratuities can claim the credit. Examples for eligible businesses include cruise ships, casino restaurants, food delivery services, and valet operations.

Start your application now to see if you qualifyTippedRefund.com is for food and beverage business owners who don't leave money on the table. Below are FICA Tip Credit Refund case study images from businesses whose owners claim back what's rightfully theirs.

No tax refund? No cost

10,000+ businesses served through programs like this

Below are some of the many questions we get from restaurant and bar owners regarding the FICA Tip Credit Refund. Feel free to skim, but know that our specialists manage every IRS requirement on your behalf anyway.

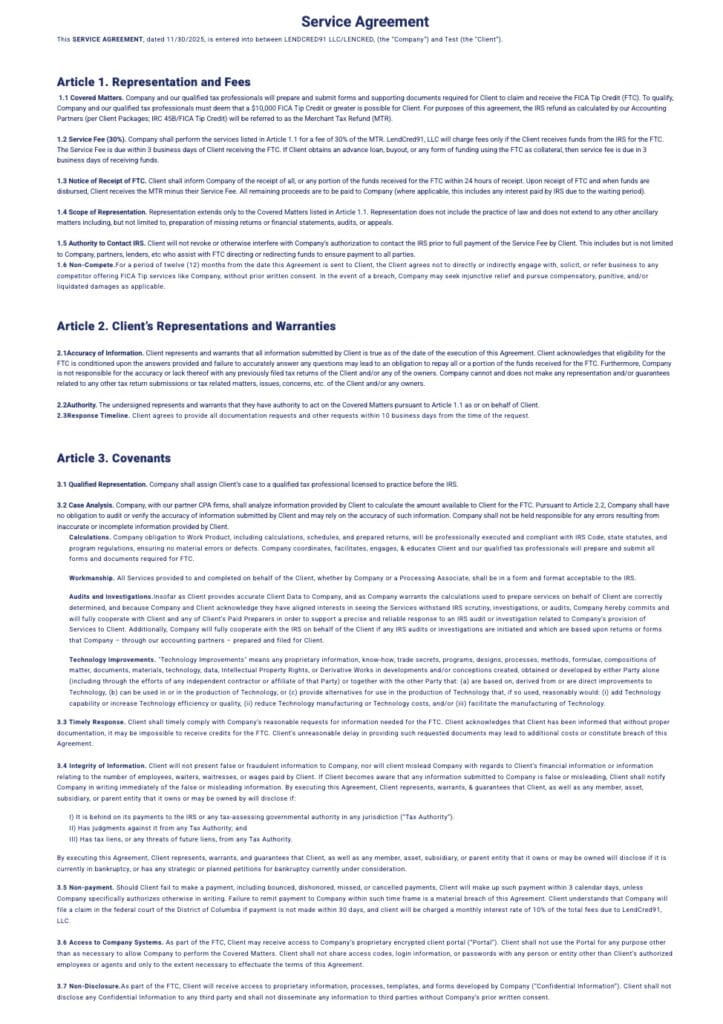

Secure your priority processing spot nowOur FICA Tip Credit Refund service at TippedRefund.com operates on a 25 % success fee basis. This means, we charge a percentage of the recovered money rather than upfront costs. This contingency model eliminates financial risk for you as a business owner. If you as a business owner don’t receive the tax refund by the IRS, you don’t pay anything, it’s that simple!

The FICA Tip Credit (IRS Code Section 45B) is a dollar-for-dollar tax credit for businesses with tipped employees. The FICA Tip Credit reduces taxable business income by the employer’s share of Social Security and Medicare taxes (FICA taxes) paid on qualifying employee tips. Eligible businesses (like restaurants, bars, and nightclubs) recover FICA taxes paid on employee tips from the last 3 years through the FICA Tip Credit Refund.

IRS Code Section 45B was approved in 1993 by the IRS for food and beverage businesses. From 2026 onwards, other tip-receiving businesses like hairdressers, nail salons, and spas become eligible for the credit. The FICA Tip Credit Refund is not a deduction. The employer tip tax credit directly reduces your tax liability, benefiting your business directly with cash flow.

The FICA Tip Credit Refund is issued by the IRS, while TippedRefund.com manages and accelerates the recovery process for business owners, getting them back paid FICA taxes with less paperwork, in less time.

FICA stands for Federal Insurance Contributions Act, the 1935 legislation establishing payroll taxes funding Social Security and Medicare. FICA taxes provide retirement income, disability insurance, survivor benefits, and healthcare coverage for Americans age 65 and older.

The combined FICA rate totals 15.3% of wages: 12.4% Social Security (split equally between employer and employee at 6.2% each) plus 2.9% Medicare (1.45% each). Social Security applies to wages up to $176,100 (2025 cap); Medicare has no ceiling.

Employer FICA payments on tip income, specifically the employer’s 7.65% share, form the basis for FICA tip credit calculations.

The FICA Tip Credit Refund equals 7.65% of qualifying tip wages paid above the federal minimum wage threshold. A restaurant with 15 tipped employees averaging $300 weekly in reported tips generates approximately $17,800 per year in tax credits. The tax refund applies retroactively for three prior tax years, creating refunds often exceeding $50,000 for businesses that never claimed this benefit.

The tip tax refund amount depends on total reported tips, hours worked, and wage structures. From our experience, higher-volume restaurants with strong tip reporting practices usually recover much more than establishments with inconsistent documentation.

Yes, most food and beverage businesses where tipping is customary qualify for the employer FICA Tip Credit. The following businesses are eligible examples.

The business must employ workers who receive tips for providing, delivering, or serving food and beverages.

No minimum employee count exists. Single-location diners with two servers and multi-unit restaurant groups with hundreds of tipped employees both qualify. The employer must pay FICA taxes on reported tip income and compensate employees at least federal minimum wage (including tips).

Non-food industries where tipping occurs (like hair salons, spas, taxi services) are eligible from 2026 onwards.

Yes, LLCs, S-Corps, and C-Corps qualify for the FICA Tip Credit. The difference lies in where the refund lands.

LLCs and S-Corps are pass-through entities. The IRS sends your refund directly to you as the business owner. C-Corps receive the refund at the business level, deposited into the corporate account.

Your entity structure affects routing, not eligibility. The credit calculation remains identical regardless of how your restaurant is organized.

Yes, businesses claim the FICA Tip Credit Refund retroactively by filing amended tax returns for up to three prior tax years. A restaurant filing in 2025 recovers credits from tax years 2022, 2023, and 2024. The three-year window follows IRS statute of limitations for refund claims. You can even claim the tipped employee refund if you sold the businesses, but were owner at the time.

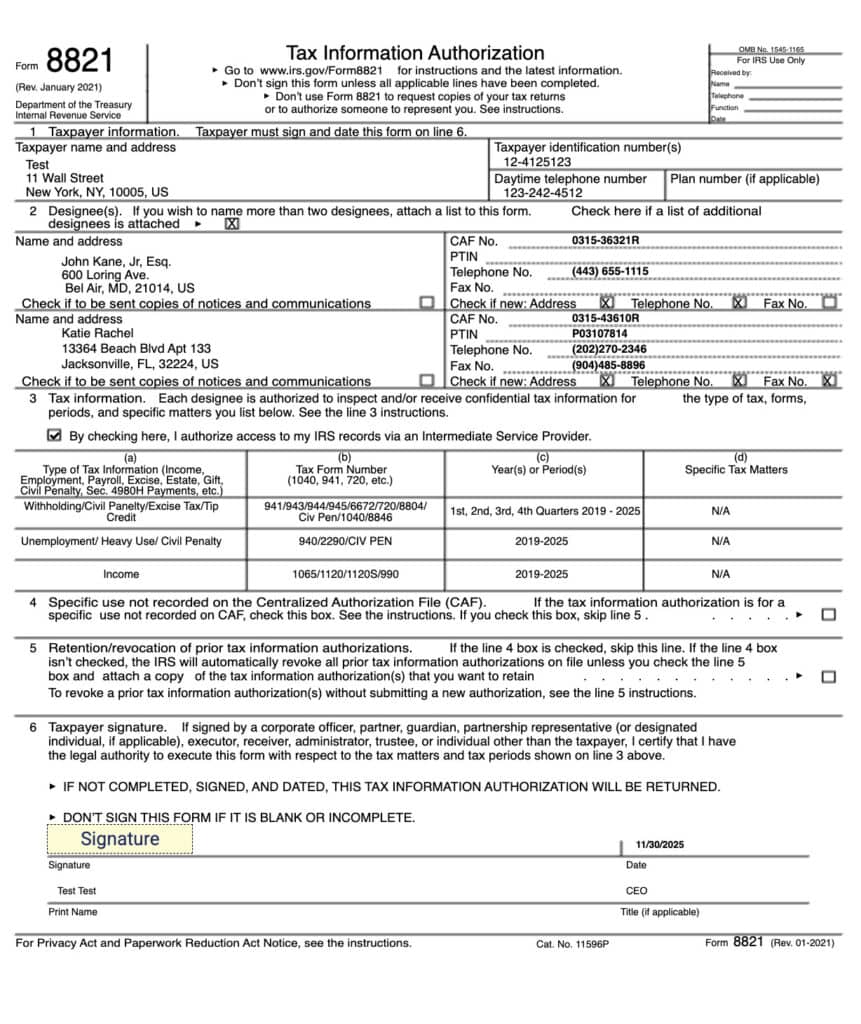

Retroactive claims require Form 8846 attached to amended returns (Form 1120-X for corporations, Form 1065-X for partnerships). The documentation standards remain identical to current-year filings. Payroll records, tip reports, and W-2 forms from prior years substantiate the claim.

Missing documentation from earlier years complicates but doesn’t necessarily prevent retroactive claims. Payroll providers retain records; POS systems store historical tip data; bank statements reconstruct wage payments. All these help.

As you can see: Usually, claiming FICA tip credit is tedious and requires a lot of paperwork from you.

At TippedRefund.com, we support business owners like you throughout the entire refund process. We pull your information from the IRS on your behalf, cutting down the time and effort to claim your tip money to a minimum. All you need to do to get started are 4 steps, taking around 4 minutes. After you’ve submitted your information, we’ll confirm everything on our end and process your claim digitally in our custom platform.

The FICA tip credit refund process takes 4 to 12 weeks from submission to payment receipt, depending on claim complexity. Current-year credits applied against tax liability process within 4-6 weeks after return filing. Amended returns requesting refunds for prior years require 8-12 weeks for IRS processing.

The initial document gathering and calculation typically requires 2-3 weeks of preparation. When working with businesses with organized payroll records and consistent tip reporting this phase is faster. Disorganized documentation usually stretches preparation to 6-8 weeks.

IRS backlogs occasionally extend standard processing times. High-volume filing periods (April-June) experience somewhat slower turnaround than off-peak months as well.

The FICA tip credit calculation uses a four-step formula based on tip income exceeding the $5.15 per hour minimum wage threshold. Start by multiplying the minimum wage basis ($5.15) by total hours worked for each employee. Subtract this amount from total reported tips. Apply the 7.65% FICA tax rate to the remaining tip balance.

Consider a server working 120 hours monthly at $2.13 per hour direct wages, reporting $1,800 in tips. The minimum wage threshold equals $618 (120 hours × $5.15). Creditable tips total $1,182 ($1,800 – $618). Monthly credit: $90.42 ($1,182 × 7.65%).

The $5.15 threshold remains frozen at the January 2007 minimum wage rate, regardless of current federal or state minimums. This locked threshold actually increases credit value over time as tip amounts grow.

The FICA Tip Credit Refund calculator we provide at the top of the page makes the process of getting a rough refund estimate easy for business owners.

Federal tip credit obligations under FLSA permit employers to pay tipped employees $2.13 per hour in direct cash wages, with tips bridging the gap to the $7.25 federal minimum wage. State law adds another layer. Seven states prohibit wage tip credits entirely: Alaska, California, Minnesota, Montana, Nevada, Oregon, and Washington. Employers in these states pay full state minimum wage before tips enter the equation.

Other states permit wage tip credits under tighter restrictions than federal rules. New York City hospitality employers pay at least $10.65 per hour in direct wages, applying only $5.35 as tip credit toward the $16.00 minimum wage. Arizona mandates $11.35 direct wages with a maximum $3.00 tip credit.

The stricter rule, federal or state, always controls the cash wage you pay. This wage obligation remains separate from the federal FICA tip tax credit. Even in “no state tip credit” jurisdictions like California, where employers pay full state minimum wage ($16.00 in 2024) and employees keep all tips, the federal FICA Tip Credit remains available on employer FICA taxes paid on reported tip income.

The FICA Tip Credit functions identically in all states because it’s a federal income tax credit claimed on IRS Form 8846. State tip credit laws (governing minimum wage calculations) remain separate from the FICA tip tax credit. Even California employers who cannot take a tip credit against minimum wage obligations still claim the full FICA tip tax credit.

Higher-wage states often generate larger FICA tip credits per employee. Workers earning $16.00 hourly plus tips report higher total compensation than employees in $7.25 states, expanding the creditable tip amount.

State income tax implications differ. Some states offer complementary credits; others require wage deduction adjustments on state returns paralleling federal rules.

Tip credit and tip offset describe the same wage calculation mechanism: counting employee tips toward minimum wage obligations. “Tip credit” is the formal FLSA terminology; “tip offset” appears in state regulations and colloquial usage. Both terms reference the amount employers deduct from cash wages because tips cover the difference.

The federal tip credit caps at $5.12 per hour ($7.25 minimum wage minus $2.13 required cash wage). States using “tip offset” language often set different thresholds. Colorado allows $3.02 tip offset against its $14.42 minimum wage.

Neither term relates to the FICA tip tax credit, which reduces income tax liability rather than wage payment requirements.

The FICA Tip Credit and Employee Retention Credit (ERC) operate as distinct tax programs with different eligibility criteria. The FICA Tip Credit is permanent, applies exclusively to food and beverage employers, and credits FICA taxes paid on tips above minimum wage. ERC was a pandemic-era program crediting 50-70% of qualified wages for businesses impacted by COVID-19 operational restrictions.

ERC expired for wages paid after September 30, 2021 (most employers) or December 31, 2021 (recovery startup businesses). New ERC claims face IRS moratorium and heightened scrutiny. The FICA tip credit remains available without sunset date for every qualifying tax period.

Businesses that claimed ERC on tipped wages cannot double-dip by claiming FICA tip credit on identical wages. Proper allocation prevents overlap.

Yes, you can still claim the FICA tip credit if you’ve previously claimed the Employee Retention Credit (ERC). The FICA Tip Credit and Employee Retention Credit are separate programs with minimal overlap. ERC ended in 2022; the §45B tip credit remains available for amended returns covering the past three years.

Previous ERC claims don’t disqualify your restaurant. Our CPA team reviews which quarters and employees were included in your ERC filing, then factors that data into your tip credit calculation. The adjustment ensures accuracy without reducing your eligibility.

Most restaurants that claimed ERC still qualify for a significant FICA Tip refund.

The FICA tip credit affects other restaurant tax credits through wage stacking limitations. Employers cannot claim multiple wage-based credits on identical compensation. Work Opportunity Tax Credit (WOTC), which rewards hiring veterans and disadvantaged workers, requires separate wage allocation from FICA tip credit calculations.

Non-wage credits combine freely. Research and Development credits, energy efficiency incentives, and accessibility modification credits stack without restriction alongside FICA tip credits.

Strategic planning maximizes total benefit. A veteran server’s wages might qualify for WOTC certification during year one, then shift entirely to FICA tip credit calculations in subsequent years once WOTC eligibility expires.

The FICA tip credit and minimum wage tip credit serve completely separate purposes despite similar names. The minimum wage tip credit (or “tip credit” under FLSA) allows employers to pay tipped workers below minimum wage, counting tips toward the difference. The FICA tip credit reduces federal income tax liability based on employer FICA taxes paid on tip income.

Taking a minimum wage tip credit reduces labor costs directly. Claiming the FICA tip tax credit reduces tax obligations at year-end. Both benefits can apply simultaneously—employers paying $2.13 hourly (using minimum wage tip credit) still claim the FICA tip tax credit on all reported tips.

California restaurants that cannot use minimum wage tip credit still access full FICA tip tax credit benefits.

No, the FICA Tip Credit is a tax credit, not a deduction. Tax credits reduce tax liability dollar-for-dollar. A $10,000 FICA Tip Credit eliminates $10,000 in federal income tax owed. Tax deductions reduce taxable income, saving only a percentage based on marginal tax rate.

A business in the 21% corporate tax bracket saves $2,100 from a $10,000 deduction. That same business saves $10,000 from a $10,000 credit—nearly five times greater benefit.

The FICA Tip Credit is a non-refundable general business credit. Unused amounts carry back one year or forward up to 20 years. Credits exceeding current tax liability aren’t lost; they apply against future obligations.

No, claiming the FICA tip tax credit does not trigger IRS audits when properly documented. Form 8846 is a standard business tax form filed by thousands of restaurants annually. The credit has existed since 1993 with established calculation methods and documentation requirements.

Your audit likelihood increases with inconsistencies. Typical examples of inconsistencies are as follows.

Maintaining organized records (tip reports, payroll summaries, Forms 941, W-2 statements) provides audit protection. Consistent documentation practices eliminate most examination concerns.

You likely weren’t told about the FICA Tip Credit Refund, because accountants prioritize compliance over recovery. Their primary function involves filing accurate returns and ensuring you pay what’s owed, not identifying refunds from past overpayments.

The IRS code contains over 2,500 business tax credits. A CPA handling your books juggles payroll, quarterly filings, depreciation schedules, and dozens of other responsibilities. Expecting mastery of every obscure credit provision is unrealistic. Picture a restaurant maintaining 2,500 menu items; no chef could execute each dish with expertise.

Section 45B tip credit recovery requires specialized knowledge that falls outside standard accounting practice. The credit calculation involves FICA taxes paid on tips exceeding minimum wage thresholds, a niche area most generalist accountants encounter rarely, if ever.

The result: 94% of eligible restaurants never file for their §45B refund. More than 90 % of the thousands of food and beverage businesses we’ve spoken to never even heard about it. Your accountant isn’t negligent. They’re simply not a FICA tax recovery specialist.

Yes, you can claim the FICA tip credit, but the refund only applies to the reported tips. Unreported cash tips generate zero credit benefit because no FICA taxes were paid on that income. Employers who improve tip reporting compliance immediately increase their creditable amount.

The IRS requires employees to report tips exceeding $20 monthly. Implementing electronic tip tracking through POS systems helps you capture more accurate data than manual reporting. Credit card tips create automatic paper trails; cash tip compliance requires employee cooperation.

Better tip reporting benefits employees through higher Social Security wages and more accurate W-2s for loan applications. Framing compliance as mutual benefit increases your voluntary reporting rates.

Yes, claiming the FICA tip credit requires reducing your wage expense deduction by the credit amount. IRS rules prevent double benefits: you cannot deduct FICA taxes as business expenses while simultaneously claiming credits for those same taxes. The deduction reduction equals the credit claimed.

This reduction still produces net tax savings. A $10,000 credit with corresponding $10,000 deduction reduction costs approximately $2,100 in lost deduction benefit (at 21% rate) while providing $10,000 in credit value—net benefit of $7,900.

The employer tip credit requires Form 8846 (Credit for Employer Social Security and Medicare Taxes Paid on Certain Employee Tips) attached to your annual business tax return. Corporations file Form 8846 with Form 1120; S-corporations with Form 1120-S; partnerships with Form 1065; sole proprietors with Schedule C on Form 1040.

Form 8846 feeds into Form 3800 (General Business Credit), which aggregates all business credits. The 3800 calculates limitations and carryforward amounts.

Retroactive claims add amended return forms: Form 1120-X (corporations), Form 1065-X (partnerships), or Form 1040-X (sole proprietors), each with Form 8846 attached.

At Tippedrefund.com, we’ll help you expedite the process and streamline it digitally, by pulling all available IRS transcripts on your behalf. Our process minimizes paperwork needed from you. Our expert CPAs will troubleshoot anything else that could come up and support you throughout the entire process in case there’s anything missing.

Employer tip credit claims require four categories of documentation.

Form 8027 filing requirements apply to establishments where tipping is customary, food/beverage operations occur, and more than 10 employees worked on a typical business day. Smaller operations may still qualify for Form 8846 without Form 8027 obligations.

Retain records for at least four years after filing. Digital backups of payroll summaries, POS tip reports, and tax filings provide audit protection without physical storage burdens.

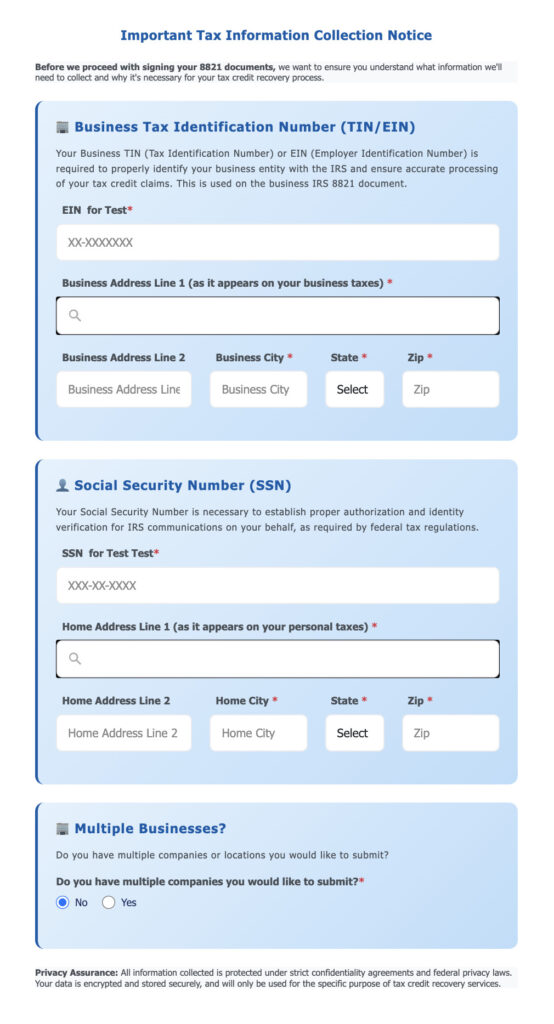

If you use TippedRefund.com, we only require your EIN and SSN for verification with the IRS, as well as signing our service agreement and automatic forms for IRS transcript access. This takes only around 4 minutes compared to trying to understand the traditional way. With our system, we process the entire refund on your behalf digitally. If anything is missing, our FICA tax specialized CPAs support you in everything needed.

Restaurant and bar owners can reduce their FICA tax burden through three primary methods.

S-corporation owners paying themselves “reasonable compensation” can take remaining profits as distributions, which bypass FICA taxation. A restaurant owner earning $150,000 might take an $80,000 salary (subject to FICA) and $70,000 distribution (not subject to FICA), saving approximately $10,700 annually.

Health insurance premiums, retirement contributions, and dependent care benefits paid through qualified plans reduce the wages subject to FICA before taxes apply.

No, FICA taxes do not reduce taxable income on employee returns. FICA withholdings come directly from gross wages without creating deductions. Employees pay federal income tax on full wages before FICA amounts are subtracted.

Employers deduct FICA taxes paid as ordinary business expenses, reducing taxable business income. The employer’s 7.65% FICA contribution on wages (including tips) lowers net profit subject to income tax.

The FICA tip credit provides additional employer benefit beyond deductibility. It’s a dollar-for-dollar tax reduction that exceeds deduction value by approximately 4-5 times.

No, a FICA Tip Credit recovery service is legitimate when claims are filed through official IRS channels, as TippedRefund.com does. The credit itself is codified in Internal Revenue Code Section 45B, established by Congress in 1993 to offset employer FICA taxes paid on employee tips.

Skepticism makes sense. After speaking with thousands of business owners, less than 10% have ever even heard about this program. Most restaurants operate for years without hearing about the credit, then we contact them promising substantial refunds. The sudden appearance of “free money” leads to reasonable suspicion.

Below, we have listed the criteria that separate legitimate recovery services from problematic ones (TippedRefund.com checks all boxes by the way).

The credit itself carries no risk. The IRS either approves your refund or denies it. Denied claims result in no refund and no cost; they don’t trigger penalties or audits when filed accurately.

TippedRefund.com is a service brand of Tip Credit Partners (LenCred).

Starting in 2026, the FICA tip credit expands beyond restaurants to include hairdressers, nail salons, spas, and other tip-receiving businesses. This legislative change opens significant tax recovery opportunities for service industries that previously had no access to this benefit.

For restaurant employers, the existing FICA tip credit already returns a substantial portion of taxes paid on employee tips. The Section 45B tax credit converts what appear to be unavoidable FICA obligations into recoverable amounts. Many restaurant owners overlook this benefit entirely; thousands of dollars go unclaimed each year as a result.

The 2026 expansion means salon owners, spa operators, and similar businesses can begin preparing documentation systems now. Tracking tip income accurately positions these employers to claim credits immediately when eligibility begins.

FICA contributions create tangible benefits for employees too. Each contribution builds Social Security credits that increase retirement and disability protection over time. Higher reported wages improve worker financial security in practical ways: employees applying for mortgages or car loans gain credibility through documented income. Tip reporting becomes a mutual advantage rather than a burden.

The permanent structure of this credit distinguishes it from temporary relief programs. Unlike pandemic-era tax benefits with expiration dates, the FICA tip credit remains available indefinitely for qualifying businesses. Establishing proper documentation practices creates sustained annual savings without the uncertainty of program sunsets.

Show all tip credit questions

No tax refund? No cost

$0 upfront cost

Fully secure

IRS-compliant